Geometric Patterns (Flags + Head & Shoulders)

Date: 2026-05-31 IST

Sources: MQL5 Price Action Analysis Toolkit

- Flags (continuation): Part 69 — https://www.mql5.com/en/articles/22503 + Flag_Pattern_Detector.mq5

- Head & Shoulders (reversal): Part 66 — https://www.mql5.com/en/articles/22194 + HS_Indicator.mq5

Archived: references/MQL5/lynnchris/implemented/Part69/ and Part66/.

Built on the shared Market Structure foundation (Part 21). Core: quantwave-core/src/indicators/geometric_patterns.rs.

The GeometricPatternScanner (exposed as .ta.geometric_patterns() in Polars) detects two high-value classical price action patterns using the confirmed swings and bias from MarketStructure:

- Bull / Bear Flags — Powerful continuation patterns. A sharp impulse "pole" followed by a shallow, orderly consolidation (pullbacks dominate pushes, retrace typically ≤ 61.8%). Breakout in the pole direction is the trigger.

- Head & Shoulders (and Inverse) — Classic reversal patterns. A 5-swing formation with a dominant head, reasonable symmetry in price and time, and a decisive neckline breakout.

Both detectors emit rich, machine-readable structs (FlagPattern, HsPattern) instead of drawing objects. These structs contain exactly the quantitative fields you need for position sizing, quality filtering, and ML.

When to Use

Flags: - Trend-following continuation entries in the direction of established MarketStructure bias. - Situations where you want quantified risk (the pole length gives you a natural ATR-multiple stop/target distance).

Head & Shoulders:

- Counter-trend reversal plays at major turning points.

- Only high-score / high-symmetry instances (filter aggressively).

General: - As confluence with S/R levels (see sr_monitor). - As sparse, high-signal labels or features for ML models. - In event-driven backtesters that consume rich metadata for dynamic sizing.

Detection rules (MQL5-faithful):

- Flags: 3-bar impulse pole (≥

min_pole_atr× ATR), consolidation with retrace ≤ 61.8%, pullbacks ≥ pushes, breakout above/below pole extreme. - H&S: 5-swing window (H-L-H-L-H or inverse), shoulder symmetry ≤ 2%, height ≥ 1.5× ATR, composite score ≥ 60.

Flags emit on breakout_confirmed only; H&S emits on high-score pattern detection (neckline breakout optional in streaming).

Rich Metadata — The Real Power

FlagPattern (key fields)

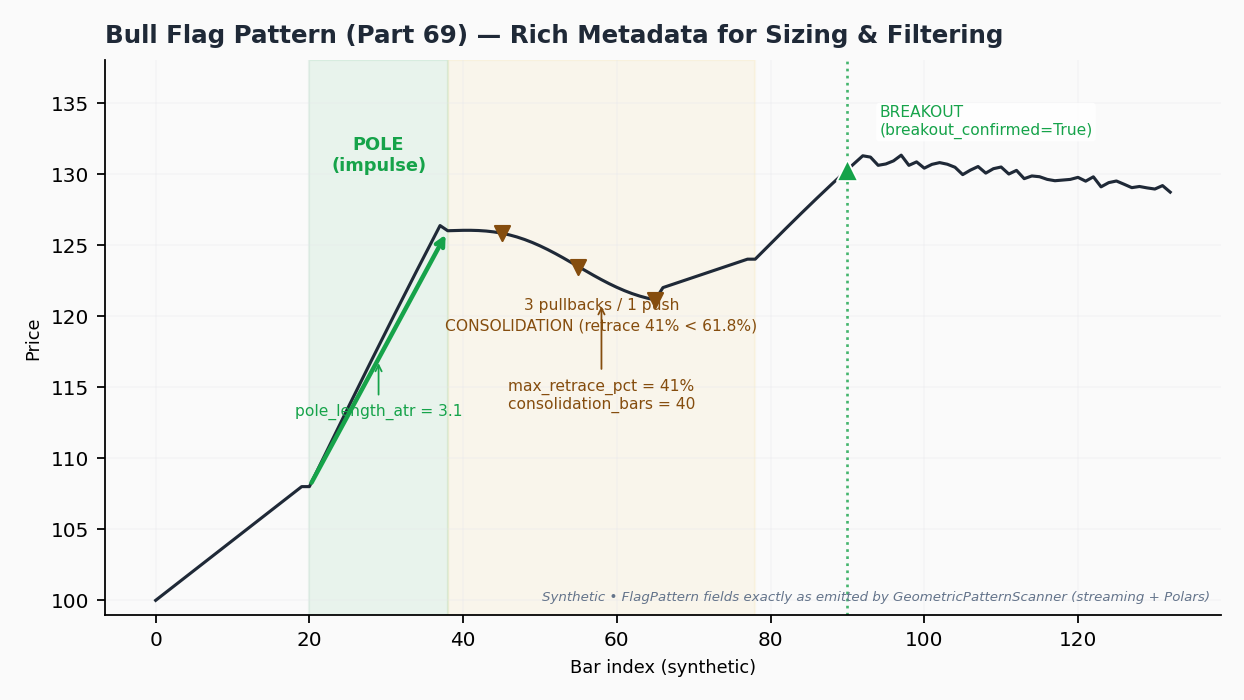

pole_length_atr: The star field for strategies. Pole height expressed in ATR units at detection time. Directly drives position sizing.max_retrace_pct: How far price pulled back during consolidation (as % of pole). Classic flags stay under 0.618.pullbacks,pushes: Count of counter-moves vs. continuation moves inside the flag. Good flags usually have more pullbacks than pushes.consolidation_bars: Duration of the flag (time consolidation).breakout_confirmed,breakout_price,is_bull

HsPattern (key fields)

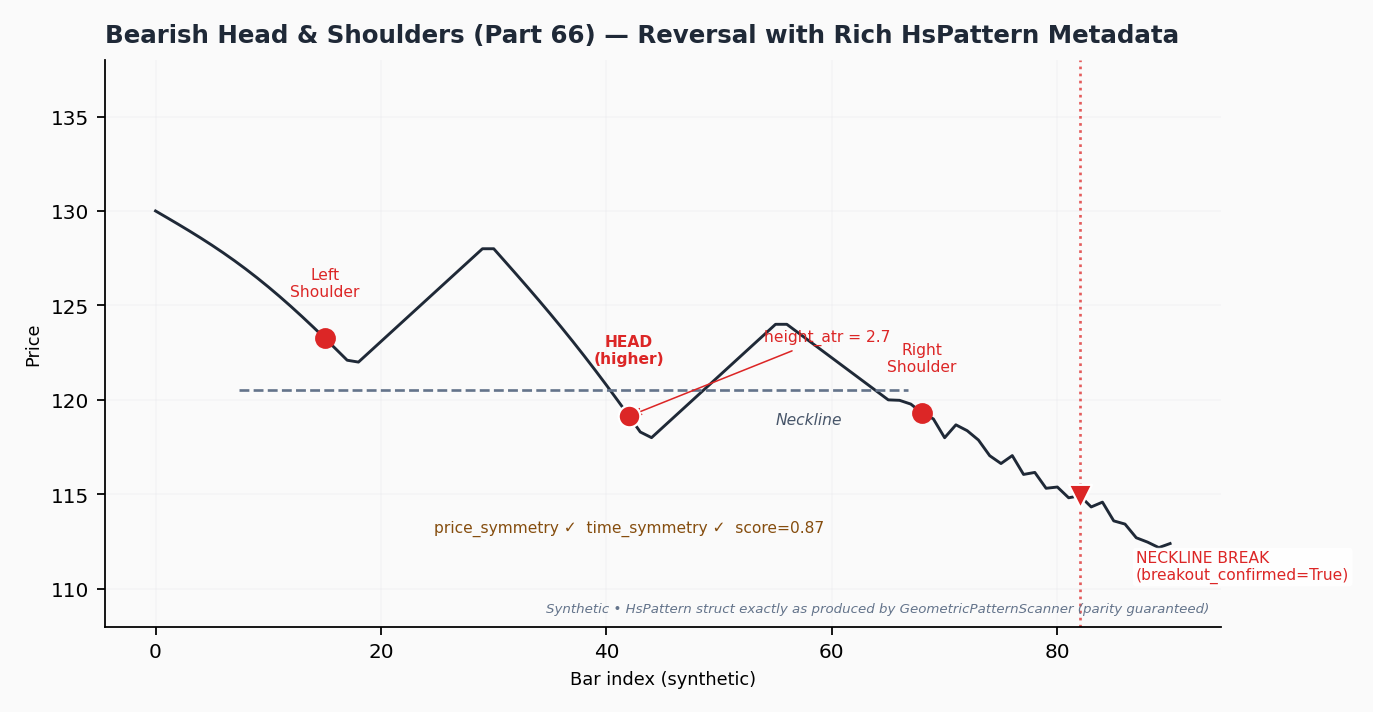

height_atr: Head height in ATR units (analogous to pole_length_atr).score: Composite quality score (0–1+). Higher is better; combine with symmetry.price_symmetry,time_symmetry: How balanced the left/right shoulders are.breakout_confirmed,breakout_price,is_bearish

Visual: Bull Flag

Sharp vertical impulse pole (e.g. bars 120–127), followed by 3 small pullbacks and 1 push inside a tight range (retracement 48%), then a decisive breakout candle above the pole high at bar 143. Annotations call out every FlagPattern field on the chart.

Visual: Bearish Head & Shoulders

Left shoulder, higher head, lower right shoulder, roughly flat or slightly declining neckline, followed by a strong close below the neckline. Labels for all five swing points, measured head height, symmetry percentages, and score.

Position Sizing Example Using Rich Metadata

# After detecting a confirmed bull flag on bullish structure

current_atr = atr_series[bar]

risk_per_unit = 0.5 * flag.pole_length_atr * current_atr # 0.5× pole as risk distance

account = 100_000.0

risk_pct = 0.01 # 1% account risk per trade

contracts = (account * risk_pct) / risk_per_unit if risk_per_unit > 0 else 0

print(f"Position size: {contracts:.1f} units (risk = {risk_per_unit:.2f})")

This produces consistent R-multiples across different instruments and volatility regimes because the risk distance is normalized by the actual pattern size.

Practical Code Examples

Rust Streaming

use quantwave_core::indicators::geometric_patterns::GeometricPatternScanner;

use quantwave_core::traits::Next;

let mut scanner = GeometricPatternScanner::new(3);

for (h, l) in data {

let (ms_state, flag, hs) = scanner.next((h, l));

if let Some(f) = flag {

if f.breakout_confirmed && ms_state.bias == Bias::Bullish {

let size = compute_size_from_pole(f.pole_length_atr, current_atr);

// enter long...

}

}

if let Some(hs_pat) = hs {

if hs_pat.breakout_confirmed && hs_pat.score > 0.75 {

// high-quality reversal setup

}

}

}

Polars Batch (ideal for feature stores)

df = (

pl.DataFrame({"high": highs, "low": lows})

.lazy()

.ta.market_structure("high", "low", 3)

.ta.geometric_patterns("high", "low", 3)

.collect()

)

# Rich nested access for ML labels / features

bull_flag_events = df.filter(

pl.col("geometric_patterns").struct.field("flag")

.struct.field("breakout_confirmed") &

(pl.col("market_structure").struct.field("bias") == "Bullish")

)

features = bull_flag_events.select([

pl.col("geometric_patterns").struct.field("flag").struct.field("pole_length_atr").alias("pole_atr"),

pl.col("geometric_patterns").struct.field("flag").struct.field("max_retrace_pct"),

# ... join other indicators at these exact bars

])

Canonical PA foundation notebook

End-to-end strategy wiring (MarketStructure filter + flag breakout + pole sizing sketch):

- pa_foundation_strategy.py

- pa_flag_breakout_strategy.py (full

.btbacktest tour)

Python Streaming

from quantwave import GeometricPatternScanner, MarketStructure

geo = GeometricPatternScanner(3)

for h, l in zip(highs, lows):

# Note: in current Python surface the scanner also advances internal MS

result = geo.next(h, l) # returns GeometricNextResult

flag = result.flag

if flag and flag.breakout_confirmed:

print(f"Flag pole_atr={flag.pole_length_atr:.2f}")

Python note: The streaming wrappers expose the core rich fields (including pole_length_atr, score, symmetry, breakout flags). For the absolute fullest metadata during research, use Polars or direct Rust.

ML & Strategy Integration Ideas

- Features:

flag_pole_atr_norm(normalized by rolling ATR or recent range)flag_retrace_quality(1 if max_retrace_pct < 0.55 else 0)hs_score,hs_symmetry_avgpattern_on_bull_structure(interaction feature)-

Binary labels for "flag breakout occurred" aligned to future returns

-

Filters: Only trade Flags when

pole_length_atr > 1.5and structure bias agrees. Only trade H&S whenscore > 0.8andtime_symmetry > 0.7. -

Confluence: Join geometric events with

SRInteractionevents on the same bar (flag breakout at major support = high edge). -

Backtester consumption: Pass the entire

FlagPattern/HsPattern(or wrappedPAEvent) into your position sizer. The metadata travels with the signal.

Full end-to-end demonstration (including regime + Hurst filter + realistic equity curve sketch) lives in the runnable notebooks.

Parameters

swing_strength(default: 3–5): Passed through to the underlyingMarketStructure. Controls swing granularity for both flags and H&S.

Metadata source of truth: GEOMETRIC_PATTERNS_METADATA constant (links directly to the two MQL5 parts).

Related Pages

- Market Structure — required foundation

- S/R Interactions — confluence

- Using Rich PA Events

- Strategy deep-dive notebook: pa_flag_breakout_strategy.md and

pa_foundation_strategy.py - MQL5 Part 69 (Flags): https://www.mql5.com/en/articles/22503

- MQL5 Part 66 (H&S): https://www.mql5.com/en/articles/22194

All detectors maintain full streaming ↔ Polars batch parity via proptests.