Market Structure (Swings + Confirmed Break of Structure)

Date: 2026-05-31 IST

Sources: MQL5 Price Action Analysis Toolkit (Part 21) — "Market Structure Flip Detector" by lynnchris. Article: https://www.mql5.com/en/articles/17891. Archived implementation: references/MQL5/lynnchris/implemented/Part21/Flip_Detector.mq5. Core implementation in quantwave-core/src/indicators/market_structure.rs (with PAEvent adapters).

Market Structure is the foundational detector in QuantWave's Price Action suite. It identifies adaptive swing points (higher-highs, higher-lows, etc.) and tracks directional bias (Bullish / Bearish / Neutral) while emitting only confirmed Break-of-Structure (BOS) flips — those that occur after bias has been established (structure count ≥ 2). This design dramatically reduces noise compared to naive swing or fractal detectors.

When to Use

- As the primary filter/gate for all other PA signals (Flags, H&S, S/R interactions).

- To establish trend regime in a clean, rule-based way without lagging moving averages.

- For high-quality entry triggers on confirmed BOS flips (e.g., first bearish flip after a series of bullish swings signals potential reversal).

- In strategies that require "structure confirmation" before acting on patterns or breakouts.

- For ML feature engineering: bias state, structure strength at events, and flip occurrences are extremely predictive when joined with regime or cycle features.

Do not use for raw every-swing signals — the confirmed-only rule is intentional (per the MQL5 Part 21 methodology).

Rich Metadata & Output

The streaming MarketStructure and Polars .ta.market_structure() both return a rich MarketStructureState (exposed as nested Struct in Polars):

bias: Bullish | Bearish | Neutral (String in Polars)last_swing_high,last_swing_low: OptionalSwingPoint{ bar, price, is_high }current_flip: OptionalFlipEvent{ is_bearish, price, bar, structure_strength }has_current_flip: Boolean convenience (Polars) for easy event filteringswing_depth_used,bar_index

FlipEvent carries structure_strength (consecutive HH/HL or LL/LH count before the breaking swing). Higher strength = more established structure before the flip.

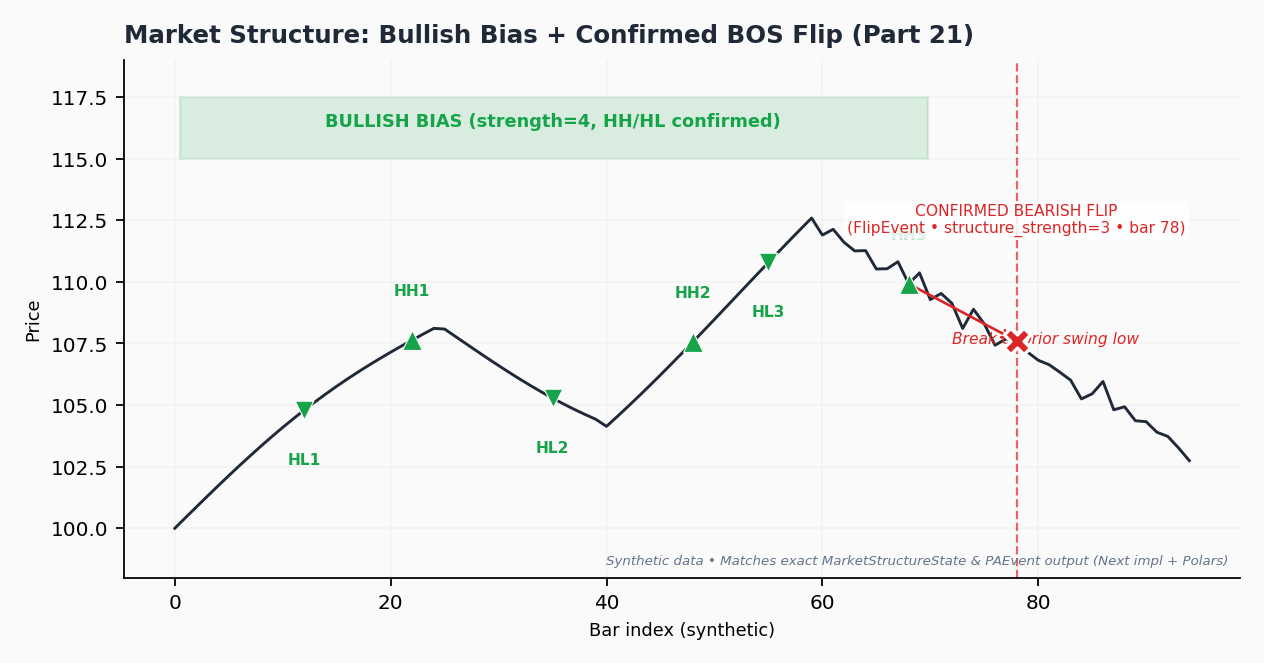

Visual: Confirmed Bullish Structure + BOS Flip

Imagine a price series making a sequence of higher highs and higher lows (e.g., swings at bars 10, 25, 40, 55). Bias turns Bullish after the second HL/HH. Later, a lower-high swing breaks the prior swing low at bar 87 — this emits a confirmed bearish FlipEvent with structure_strength=4. Only this high-quality flip is surfaced; earlier noisy swings are ignored.

See also the fuller annotated examples and code in the Price Action Patterns guide. Visual generated as part of the p1k6 documentation professionalization effort.

Practical Code Examples

Rust Streaming (Next trait — single source of truth)

use quantwave_core::indicators::market_structure::MarketStructure;

use quantwave_core::traits::Next;

let mut ms = MarketStructure::new(3); // swing_strength = 3 (common default; matches many MQL5 examples)

for (h, l) in highs.iter().zip(lows.iter()) {

let state = ms.next((*h, *l));

if let Some(flip) = &state.current_flip {

if state.bias == quantwave_core::indicators::market_structure::Bias::Bullish {

// High-quality bearish BOS flip after established bullish structure

println!("Confirmed BOS flip at bar {} (strength {})", flip.bar, flip.structure_strength);

}

}

}

Polars Batch (research, feature generation, backtesting)

import polars as pl

import quantwave as qw # or from polars import col; use .ta() extension

df = (

pl.DataFrame({"high": highs, "low": lows})

.lazy()

.ta.market_structure("high", "low", swing_strength=3)

.collect()

)

# Extract only bars with confirmed flips (the events)

flips = df.filter(

pl.col("market_structure").struct.field("has_current_flip")

)

# Rich access

print(flips.select([

pl.col("market_structure").struct.field("bias"),

pl.col("market_structure").struct.field("current_flip").struct.field("structure_strength"),

]))

Python Streaming (convenience wrapper, parity with Rust)

from quantwave import MarketStructure

ms = MarketStructure(3) # swing_strength

for h, l in zip(highs, lows):

state = ms.next(h, l) # returns MarketStructureStateResult (bias as int: 0=Neutral,1=Bullish,2=Bearish)

if state.current_flip:

print(f"Flip at bar {state.current_flip.bar}, strength={state.current_flip.structure_strength}")

Note on Python bindings: Bias is encoded as integer for FFI (0/1/2). Full rich structs (including all SwingPoint/FlipEvent fields) are available. For maximum field richness in research, prefer the Polars path.

Strategy Integration Example (Sizing & Filtering)

Use Market Structure as the bias gate:

# Pseudocode inside your strategy loop or Polars expression

if (state.bias == "Bullish" and

flag.breakout_confirmed and

recent_flip is None): # avoid entering right on a structure flip

# Proceed with long flag breakout

pass

See the companion notebook for complete examples combining with geometric patterns and regime filters.

ML / Feature Engineering Ideas

ms_bias_bullish(boolean or one-hot)structure_strength_at_event(from last flip or current state)bars_since_last_flipis_bullish_structure(derived from consecutive counts)- Event-aligned joins: at every BOS flip bar, pull concurrent values of Trendflex, Hurst, HMM regime probability, etc.

Because of guaranteed streaming ↔ batch parity (proptests in quantwave-core/tests/), features engineered on historical Polars batches transfer directly to live streaming inference with zero drift.

Parameters

swing_strength(default: 3): Radius (in bars) for local extremum detection. Higher values produce smoother, less frequent swings. (In the original MQL5 Part 21, this is often derived dynamically from ATR × multiplier; the fixed-bar version here ensures clean streaming parity while remaining highly effective.)

Metadata source of truth: MARKET_STRUCTURE_METADATA in market_structure.rs (includes LaTeX sketch of swing logic and formula_source link).

Related

- Geometric Patterns (Flags + H&S) — built directly on this foundation

- S/R Interactions

- Using Rich PA Events for Strategies & ML

- Main strategy notebook: Price Action Patterns: Market Structure, Flags, H&S, S/R

- MQL5 Part 21 (foundation): https://www.mql5.com/en/articles/17891

- Full native indicators list: Native Indicators index

All PA components ship with property-based tests asserting bit-identical results between streaming and batch replay.