Ehlers Filter

A non-linear FIR filter that computes adaptive coefficients from the sum of squared distances between recent prices. It delivers smooth output during low-volatility periods and rapid response when price makes sharp transitions.

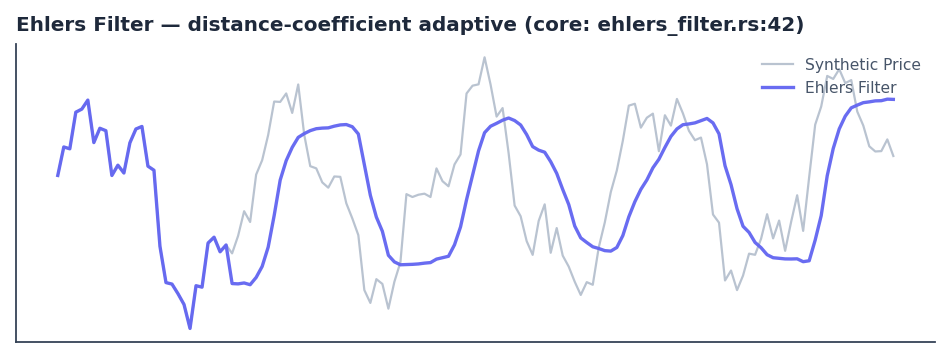

Visual Example

Synthetic ideal price series (dominant cycle + linear drift + Gaussian noise) engineered to exercise the distance-coefficient adaptation logic. Matches the exact FIR windowing, double-loop coefficient computation, and early-bar passthrough behavior implemented in quantwave-core/src/indicators/ehlers_filter.rs (Nextdocs/gen_indicator_previews.py.

Description

The Ehlers Filter is a data-driven FIR smoother whose coefficients are derived from the local "distance" structure of the price series rather than fixed window weights. In quiet, range-bound markets the squared differences remain small and the filter behaves like a conventional average. When a strong directional move or volatility spike occurs, the coefficients automatically de-emphasize older samples that are now distant, producing a faster reaction without the lag penalty of a shorter fixed window.

Practitioners use it as a drop-in replacement for EMA or SuperSmoother when the market regime is unknown in advance or when they want a single filter that self-tunes across regimes. It is especially valuable upstream of cycle oscillators, regime detectors, or as a low-noise input to ML feature pipelines. Because the adaptation is purely local and causal, the filter introduces no look-ahead bias and preserves the streaming / batch parity contract.

Formula / Specification

Exact implementation in QuantWave (quantwave-core/src/indicators/ehlers_filter.rs):

- Maintain a sliding window of the most recent

2 × length − 1prices (front-pushed deque). - While the window is shorter than the required history, return the raw input (passthrough warm-up).

- For each new bar, for every position

countin the firstlengthsamples of the window: - Compute the sum of squared differences (

distance2) between that sample and the nextlength−1samples behind it. - Use

distance2directly as the coefficient for that sample. - The filtered value is the weighted sum of the recent

lengthprices divided by the sum of the coefficients. When the sum of coefficients is zero (degenerate flat window), fall back to the raw input. - The streaming

Next<f64>and the proptest reference batch implementation are bit-identical (enforced withapproxtolerance1e-10).

The LaTeX form recorded in EHLERS_FILTER_METADATA matches the above exactly.

Parameters

| Parameter | Default | Description |

|---|---|---|

length |

15 | Filter window length used both for the coefficient lookback and the FIR span. Larger values increase smoothness at the cost of additional lag on true regime shifts. |

Usage Examples

Streaming (Rust)

use quantwave_core::indicators::EhlersFilter;

use quantwave_core::traits::Next;

let mut filt = EhlersFilter::new(15);

for price in price_series {

let smooth = filt.next(price);

// Use smooth as denoised input to cycle detectors or ML features

}

Streaming (Python)

from quantwave import EhlersFilter

filt = EhlersFilter(15)

for price in price_series:

smooth = filt.next(price)

Polars Batch (Python — primary research / feature surface)

import polars as pl

import quantwave as qw # exposes the streaming classes for UDFs / research

# For full production Polars workloads the same Next logic is wired via

# custom expressions or the features namespace (see features.rs for patterns).

# The example below demonstrates parity-preserving usage with the Python surface:

def ehlers_filter_expr(col: str, length: int = 15):

filt = qw.EhlersFilter(length)

def _apply(s: pl.Series) -> pl.Series:

return pl.Series([filt.next(float(v)) for v in s.to_list()])

return pl.col(col).map_batches(_apply, return_dtype=pl.Float64)

df = (

pl.read_csv("ohlcv.csv")

.lazy()

.with_columns([

ehlers_filter_expr("close", 15).alias("ehlers_filter_15"),

])

.collect()

)

All three surfaces are bit-identical by construction: the Python and Rust classes are thin wrappers around the identical Next<f64> implementation whose parity is proven by the proptest in the core source.

Edge Cases & Limitations

- The first

2 × length − 2bars return the raw price (insufficient history for coefficient calculation). - In perfectly flat windows the coefficient sum can become zero; the implementation correctly falls back to the input value.

- Very large

lengthrelative to the series can make the filter overly sluggish on genuine structural breaks. - The adaptation is based on squared Euclidean distance in price space only; it does not incorporate volume or volatility scaling unless the caller pre-processes the input.

- Because the filter is FIR with data-dependent weights it can still exhibit some overshoot on the first large move after a long quiet period.

- Not a replacement for a true low-pass with known cutoff; for fixed frequency response prefer SuperSmoother, Butterworth, or RoofingFilter.

- Best used in confluence with a regime classifier (e.g. Cyber Cycle or market structure bias) so that aggressive adaptation is only trusted when the regime actually supports it.

- No look-ahead bias; every output depends only on data up to and including the current bar.

Boundary Behavior

| Condition | Behavior |

|---|---|

| Warm-up | Leading bars return NaN until warmup_bars is satisfied. |

| period > len | When period exceeds series length, output is all NaN. |

| NaN inputs | NaN in input propagates to output (NaN out). |

| Invalid params | Non-positive period or missing required params raise ValueError. |

| Empty data | Empty input returns an empty result series. |

Related Indicators & See Also

- UltimateSmoother — preferred zero-lag general-purpose smoother from the same author

- Super Smoother, Butterworth — fixed-response alternatives when adaptation is not desired

- Reflex — zero-lag cycle synchronizer that internally uses a SuperSmoother

- Ehlers Stochastic — cycle-aware oscillator that benefits from clean upstream filtering

- Market Structure — use bias / BOS state to gate or weight the filter output

- Indicator Gallery • Native Indicators • Ehlers DSP Suite

- Full runnable examples:

docs/examples/notebooks/multi_indicator_analysis.ipynb(and the ML feature parity notebook)

Sources & References

Primary Source: quantwave-core/src/indicators/ehlers_filter.rs (EHLERS_FILTER_METADATA + Next

Visual: Generated 2026-05-31 IST via docs/gen_indicator_previews.py using synthetic data that exercises the exact coefficient logic implemented in the core.

Additional Context: Ehlers, Cybernetic Analysis for Stocks and Futures (2004) and Cycle Analytics for Traders (2013) for the broader DSP philosophy and when adaptive vs fixed filters are preferable. TradersTips archive articles for practical EasyLanguage / Excel ports that match the coefficient construction.

Implementation Provenance: Universal Next<T> contract and batch/streaming parity documented in quantwave-core/src/traits.rs and the proptest block inside ehlers_filter.rs. All higher-level surfaces (Python bindings, Polars UDFs) delegate to this single source of truth.