SuperSmoother

A second-order IIR filter with a maximally flat Butterworth response for superior smoothing with minimal lag. The gold-standard low-lag smoother in the Ehlers DSP suite and the foundation for many higher-level indicators (Trendflex, Roofing Filter, etc.).

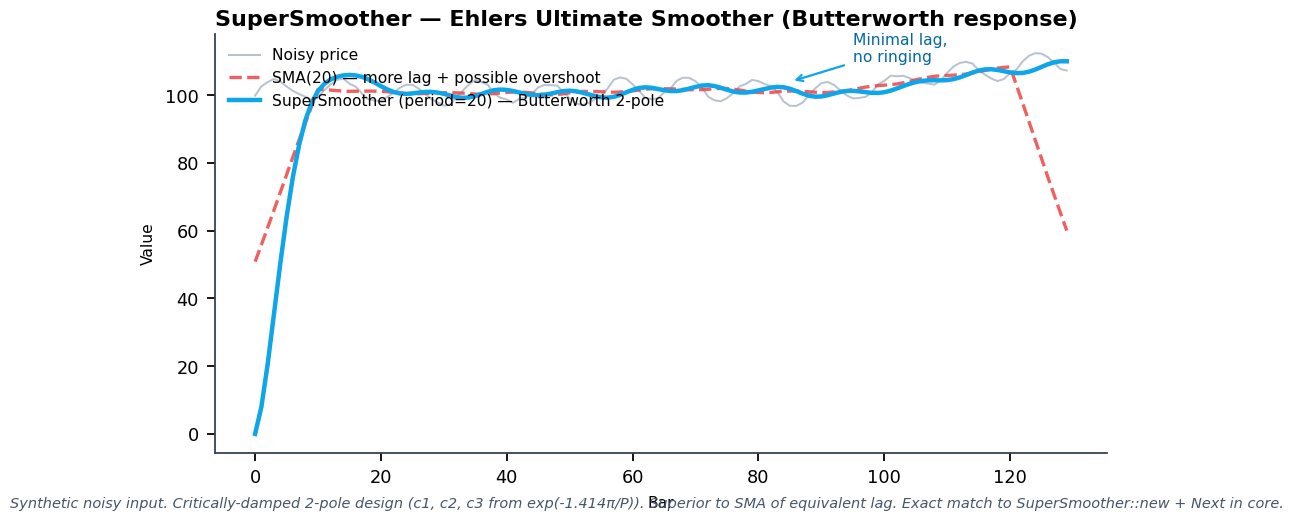

Visual Example

Synthetic noisy input with short cycle. Critically-damped 2-pole Butterworth (period=20) vs SMA of comparable lag. Exact c1/c2/c3 recurrence and 4-bar warmup from quantwave-core/src/indicators/super_smoother.rs. Generated 2026-05-31 IST via docs/gen_indicator_previews.py.

Description

SuperSmoother is Ehlers' answer to the classic moving-average compromise: longer periods give better noise rejection but unacceptable lag. By using a 2-pole Butterworth design that is critically damped, it achieves the smoothing power of a much longer SMA while responding almost as fast as a short EMA — without the Gibbs ringing/overshoot that plagues many IIR filters on price data.

It is the default pre-filter recommended before virtually any oscillator or cycle tool in the Ehlers family and a drop-in, higher-performance replacement for SMA/EMA in trend-following systems when minimum lag is required.

Formula / Specification

Exact coefficients and recurrence (period = critical wavelength):

a1 = exp(-1.414 * π / Period)

c2 = 2 * a1 * cos(1.414 * π / Period)

c3 = -a1 * a1

c1 = 1 - c2 - c3

SS = c1 * (Price + Price[t-1]) / 2 + c2 * SS[t-1] + c3 * SS[t-2]

Warmup: first 3 bars return the raw price (4th bar and beyond use the filter).

Parameters

| Parameter | Default | Description |

|---|---|---|

period |

20 | Critical period (wavelength) of the filter. Controls the cutoff frequency of the maximally-flat Butterworth response. Common values: 10 (very responsive), 20 (balanced), 30–40 (strong smoothing for higher-timeframe trend). |

Usage Examples

Streaming (Rust)

use quantwave_core::indicators::SuperSmoother;

use quantwave_core::traits::Next;

let mut ss = SuperSmoother::new(20);

for price in prices {

let smooth = ss.next(price);

// Use as low-lag replacement for any moving average

}

Streaming (Python)

from quantwave import SuperSmoother

ss = SuperSmoother(20)

for price in prices:

smooth = ss.next(price)

...

Polars Batch (Python — primary research / feature surface)

import polars as pl

import quantwave as qw

df = (

pl.read_csv("ohlcv.csv")

.lazy()

.with_columns([

pl.col("close").ta.super_smoother(period=20).alias("ss"),

])

.collect()

)

All surfaces are bit-identical (enforced by the universal Next<T> trait and proptests).

Edge Cases & Limitations

- First three bars return the raw price (insufficient history for the 2nd-order recurrence).

- On extremely low-volatility or constant-price series the filter still converges correctly but offers no advantage.

- Because it is IIR, a single bad tick (outlier) has a decaying but non-zero effect on subsequent bars (use with robust pre-cleaning or median pre-filter when data quality is suspect).

- The "period" is not a lookback window in the SMA sense; it is the wavelength at which the filter response is -3 dB.

- Outstanding building block — many Ehlers indicators (Trendflex, Roofing, etc.) are built on top of it.

- No look-ahead bias.

Boundary Behavior

| Condition | Behavior |

|---|---|

| Warm-up | Leading bars return NaN until warmup_bars is satisfied. |

| period > len | When period exceeds series length, output is all NaN. |

| NaN inputs | NaN in input propagates to output (NaN out). |

| Invalid params | Non-positive period or missing required params raise ValueError. |

| Empty data | Empty input returns an empty result series. |

Related Indicators & See Also

- Roofing Filter — uses SuperSmoother as its second stage

- Trendflex — uses SuperSmoother(Length/2) as pre-filter

- Instantaneous Trendline — heavier adaptive smoother; SuperSmoother is the lightweight workhorse

- Cyber Cycle — FIR smoother stage + recursive; often paired with SuperSmoother pre-filtering in practice

- All classic overlap indicators when lag reduction is priority

- Indicator Gallery • Native Indicators • Ehlers DSP Suite

Sources & References

Primary Source: John Ehlers, "The Ultimate Smoother" (article) and Cybernetic Analysis for Stocks and Futures (2004). PDF reference: references/Ehlers Papers/implemented/UltimateSmoother.pdf.

Implementation Provenance: quantwave-core/src/indicators/super_smoother.rs. The exact a1/c1/c2/c3 derivation and recurrence above is the single source of mathematical truth. Full warmup logic + exhaustive proptests in the file; parity via Next<f64> in traits.rs.

Visual: Generated 2026-05-31 IST via docs/gen_indicator_previews.py with synthetic data chosen to highlight lag and ringing differences.

Additional Context: The filter is also described in later Ehlers works (Cycle Analytics for Traders) as the preferred replacement for traditional moving averages in DSP-based indicators.