Trendflex

A zero-lag trend indicator that retains the trend component by measuring the normalized cumulative deviation of a SuperSmoother-filtered price from its recent history. Companion to Reflex (which removes the trend slope to isolate the cycle).

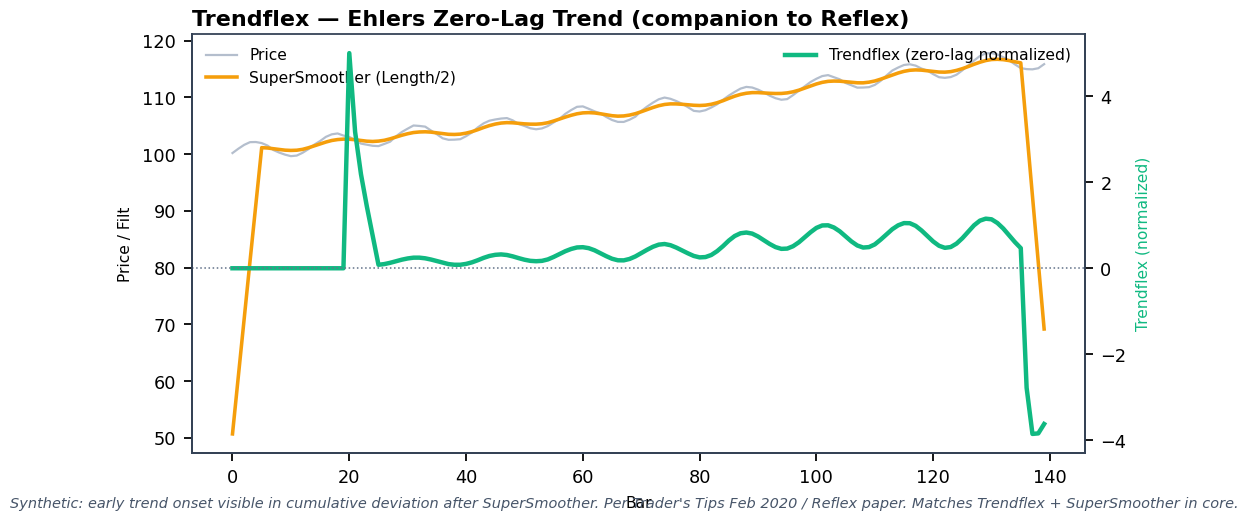

Visual Example

Synthetic ideal showing early trend detection via cumulative smoothed deviation after SuperSmoother(Length/2). Matches the exact Filt + Sum + MS normalization in quantwave-core/src/indicators/trendflex.rs (and its dependency on SuperSmoother). Generated 2026-05-31 IST via docs/gen_indicator_previews.py.

Description

Trendflex provides a near-zero-lag measurement of trend strength and direction. By first applying the SuperSmoother (a critically-damped Butterworth filter) at half the assumed cycle length, it removes high-frequency noise while preserving the trend slope. The subsequent summation of deviations from the recent smoothed history, normalized by a running mean-square, produces an oscillator-like output that leads conventional moving averages at the start of sustained moves.

It is the natural counterpart to Reflex: use Trendflex to stay with the trend and Reflex (or Cyber Cycle) to detect when the cycle component is re-asserting itself. The single tunable length parameter represents the "assumed cycle period" and is used only to size the SuperSmoother; the normalization makes the output relatively scale-free.

Formula / Specification

Exact steps (from the reference implementation):

Filt = SuperSmoother(Price, Length / 2)- Maintain a rolling history of

Filt. For each bar after warmup:Sum = (1 / Length) * Σ (Filt_t - Filt_{t-n})for n = 1..Length MS = 0.04 * Sum² + 0.96 * MS_{t-1}(exponential variance estimate)Trendflex = Sum / sqrt(MS)(or 0 when MS is negligible)

[ Filt = ext{SuperSmoother}(Price, Length/2) ] [ Sum = rac{1}{Length} \sum_{n=1}^{Length} (Filt_t - Filt_{t-n}) ] [ MS = 0.04 \cdot Sum^2 + 0.96 \cdot MS_{t-1} ] [ Trendflex = rac{Sum}{\sqrt{MS}} ]

Parameters

| Parameter | Default | Description |

|---|---|---|

length |

20 | Assumed cycle period. Controls the SuperSmoother pre-filter (internally period = length / 2). Larger values increase smoothness at the cost of slightly more lag on very long trends. |

Usage Examples

Streaming (Rust)

use quantwave_core::indicators::Trendflex;

use quantwave_core::traits::Next;

let mut tf = Trendflex::new(20);

for price in prices {

let val = tf.next(price);

// Positive and rising → strong new trend; use for direction + strength gating

}

Streaming (Python)

Polars Batch (Python — primary research / feature surface)

import polars as pl

import quantwave as qw

df = (

pl.read_csv("ohlcv.csv")

.lazy()

.with_columns([

pl.col("close").ta.trendflex(length=20).alias("trendflex"),

])

.collect()

)

All surfaces are bit-identical (enforced by the universal Next<T> trait and proptests).

Edge Cases & Limitations

- Returns 0.0 during the first

length + 1bars (history fill). - The normalization (division by sqrt(MS)) can produce large spikes when MS is near zero (very quiet markets); clamp or require minimum variance in production.

lengthshould be chosen to match the dominant cycle of the instrument/timescale; 14–30 is typical for daily/4h equities and futures.- Because it relies on SuperSmoother, any instability in the pre-filter (rare) propagates.

- Excellent for feature engineering (monotonic rising values often precede sustained moves); pair with volatility or volume filters.

- No look-ahead bias.

Boundary Behavior

| Condition | Behavior |

|---|---|

| Warm-up | Leading bars return NaN until warmup_bars is satisfied. |

| period > len | When period exceeds series length, output is all NaN. |

| NaN inputs | NaN in input propagates to output (NaN out). |

| Invalid params | Non-positive period or missing required params raise ValueError. |

| Empty data | Empty input returns an empty result series. |

Related Indicators & See Also

- Reflex — the cycle-extraction sibling (removes trend slope)

- SuperSmoother — the critical pre-filter used internally

- Instantaneous Trendline — fully adaptive (no length param) alternative

- Cyber Cycle, Roofing Filter — cycle isolation tools that complement trend measures

- Market Structure (Swings + BOS) — confirm trend direction with structure before acting on Trendflex slope

- Indicator Gallery • Native Indicators • Ehlers DSP Suite

- Strategy notebooks:

docs/examples/notebooks/pa_flag_breakout_strategy.md

Sources & References

Primary Source: John Ehlers, "Reflex: A New Zero-Lag Indicator" (2020 article). Published in Trader's Tips, February 2020. HTML reference: references/traderstipsreference/implemented/TRADERS' TIPS - FEBRUARY 2020.html.

Implementation Provenance: quantwave-core/src/indicators/trendflex.rs (depends on SuperSmoother). The exact Sum + MS recurrence above is the single source of mathematical truth. Parity proptests and Next<f64> contract in the same file + traits.rs.

Visual: Generated 2026-05-31 IST via docs/gen_indicator_previews.py with synthetic data exercising the cumulative deviation path.

Additional Context: Cross-referenced against Ehlers' later Cycle Analytics writings and multiple MQL5 ports of the Reflex/Trendflex pair.